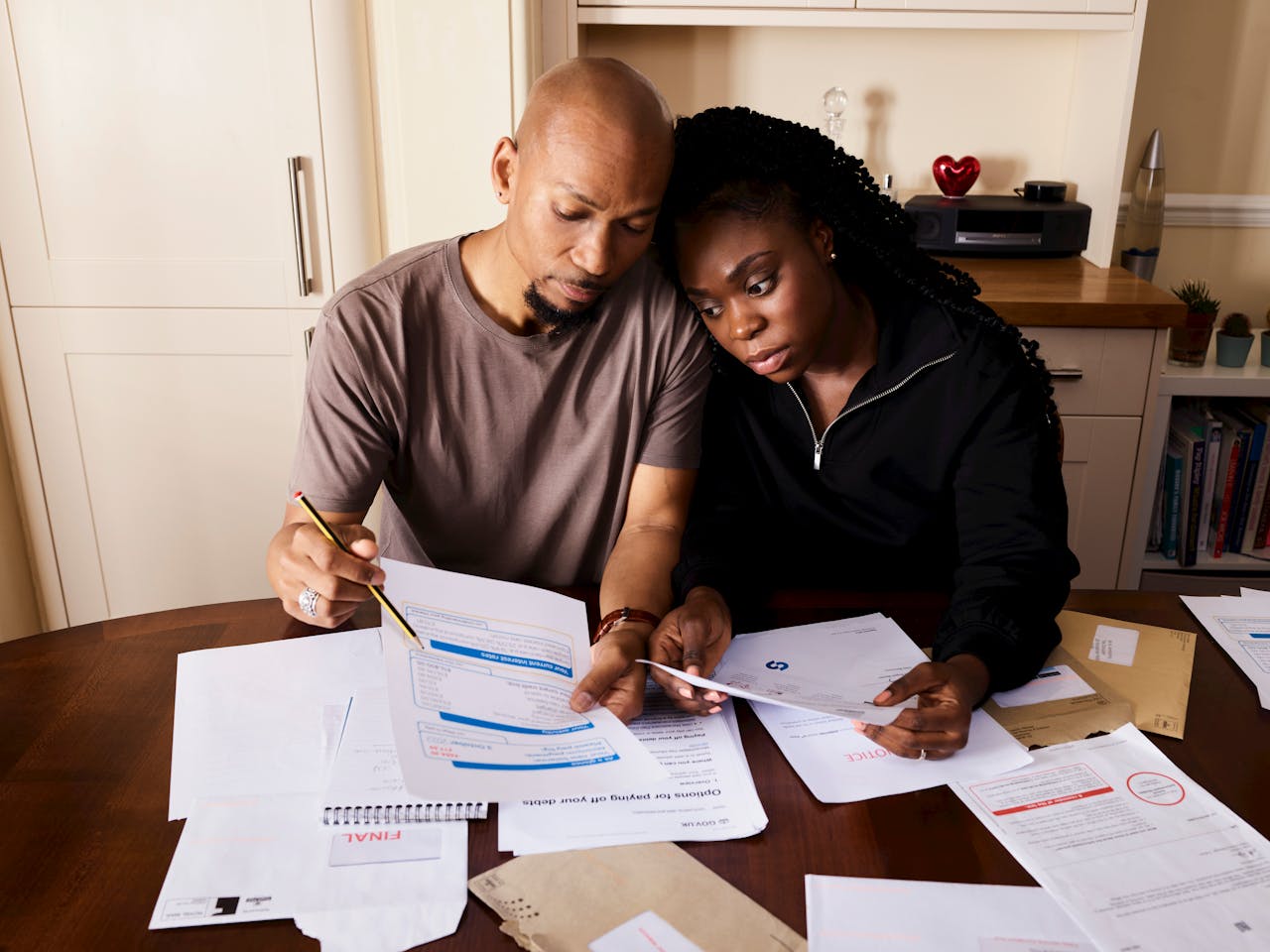

Understanding Your Challenges

Many individuals struggle with financial literacy and transparency. Identifying these challenges is the first step towards empowerment.

Tailored Solutions for Your Needs

We offer an array of services focused on improving financial literacy and providing support for those affected by institutional abuse. Partnering with Chamberlains, a leading Australian law firm, we ensure access to expert legal guidance. Dive into our resources today.

Financial Literacy

Interactive courses designed to enhance financial understanding. We provide resources that cater to all levels of expertise. Gain the knowledge you need to make informed decisions.

Institutional Advocacy

Support for individuals affected by economic misconduct. We advocate for fairness and accountability in financial systems. Our mission is to ensure your voice is heard.

Resource Center

A hub for accessible financial resources and guides. We offer a wealth of information for individuals seeking to improve their economic knowledge. Discover tips, articles, and tools to aid your journey.

Our Journey Towards Empowerment

Together, We Can Transform Lives and Futures!

Blog

Retirement Planning Advice Melbourne for Business Owners Who Want More Control Over Their Future

This is not just about pensions. It is about timing, tax, succession, and protecting personal…

How a Financial Advisor Beaumaris Can Help Families Preserve Wealth and Plan With Confidence

The right advice also creates structure. With a financial advisor Beaumaris, families can align cash…

De Facto Separation QLD: Rights & 2026 Time Limits Guide

Ending a long-term relationship is a significant life event, particularly for the high density of…

Leasehold nuances and planning rules shaping canberra conveyancing

What Makes Conveyancing in Canberra Unique? Canberra conveyancing is different from other parts of Australia…

Risk management trends among sydney conveyancing solicitors in 2026

What Are the Key Risk Management Trends Among Sydney Conveyancing Solicitors in 2026? Sydney conveyancing…

Sydney Retirement Planning Advice for High-Income Earners

Introduction: Unique Challenges for High-Income Sydney Residents High-income earners in Sydney face distinct challenges when…

Unlock Your Financial Potential

By engaging with Idea Economics, you’ll gain access to invaluable insights and support geared towards enhancing your financial capabilities.

Informed Decisions

Receive the knowledge needed to make informed financial choices that positively impact your future and well-being.

Supportive Community

Join a community of like-minded individuals working through similar challenges, offering support and understanding along the way.

Resources Galore

Access a wealth of educational resources, guides, and advocacy tools that empower you to take charge of your financial journey.